HealthSurgeon - Healthy Living and Fitness - Purium Coupon

Primary Navigation Menu

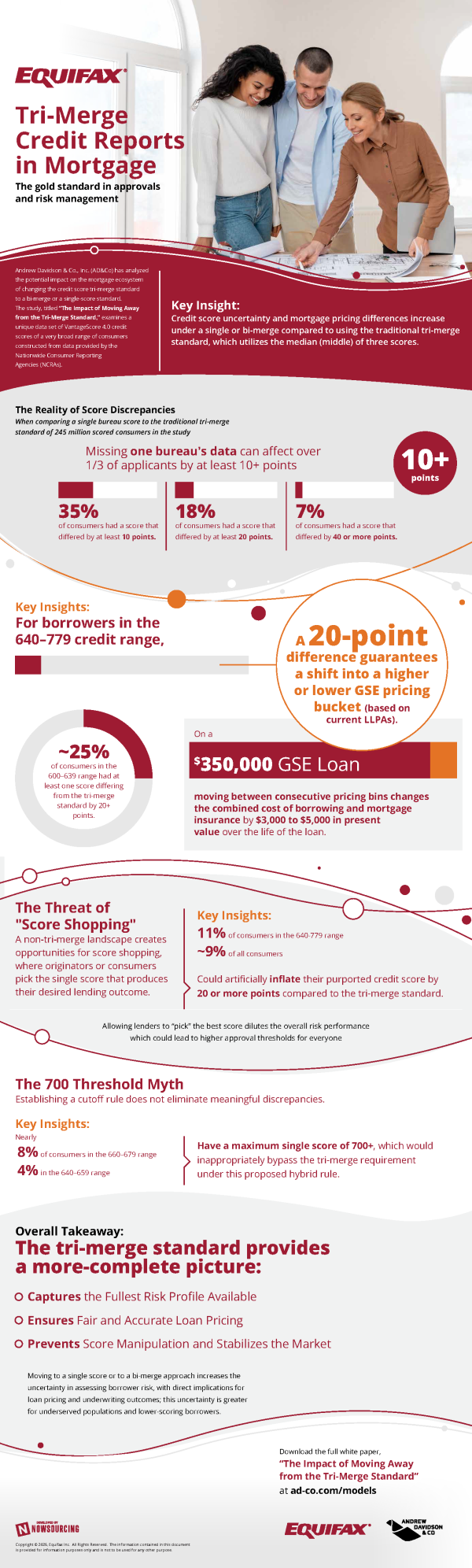

Why Credit Report Type Matters For Lenders

When it comes to pricing a loan, there are a plethora of calculations and models needed to get an accurate price. Factors like market volatility, financial forecast, risk appetite, and many more are all considered and heavily involved in the loan process. Another key component is going to the prospective borrower’s financial history, current status, and overall information. To ensure that a borrower is properly financially assessed, lenders created the standard of the tri-merge credit report.

This type of credit report works by utilizing Equifax, TransUnion, and Experian in unison. By getting information from 3 sources, you heavily cut down on bias or the possibility of one credit score being higher or lower than reality. Once you get the information from all 3 sources, you take the credit score that is the median, or the middle, of the 3. Because there are only 3 major credit bureaus, it also ensures that every lender should arrive at the same number. However, some lenders are shifting toward a bi-merge standard instead, which only utilizes 2 of the 3 bureaus.

This shift does come with its own set of problems however. By only comparing 2 scores, the possibility of extreme bias is much more present. In fact, it is estimated that eliminating data from one bureau resulted in as much as 35% of consumers having a score that differed by at least 10 points and 18% having a score difference of at least 20. While this may seem small, it can displace a borrower into the wrong pricing bucket, making loans inappropriately priced for the borrower or lender.

Ultimately, because of the risks, getting a complete financial picture is fair to both the lender and the borrower. To minimize bias and ensure that everything is being accounted for, lenders should rely on the tri-merge credit standard.

An Equifax infographic explains why tri-merge credit reports remain the gold standard for mortgage lending. It highlights how single-score models can increase pricing risk and score discrepancies.

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these cookies, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may have an effect on your browsing experience.